A second development that has risen in popularity and profitability is the investment in bitcoin mining firms, which has become an enormously popular and profitable trend for investors seeking to get exposure to the sector without actually owning the currency. In the first half of this year, several assets have outperformed bitcoin, sometimes by a wide margin.

In reality, since these firms are included in mutual funds provided by asset managers such as BlackRock, Vanguard, and Fidelity, a substantial number of investors already hold shares in these companies, maybe without even realizing it. Because of a variety of factors, including the premium they receive for being easily accessible on mainstream bourses as well as the income anticipations that come from having the insight and monetary support to buy the always-in-short-supply mining equipment, much of which is designed and built with multi-month lead times, the effectiveness of these stocks has diverged from bitcoin and even famous crypto stocks such as Coinbase and MicroStrategy recently.

It also assists that the majority of these enterprises are situated in North America, which has reaped significant benefits as a result of China’s decision to relocate practically all of its mining capacity. In fact, the United States has surpassed China as the world’s biggest mining hub, something that would have been unthinkable only a few months ago. However, these explanations are just for macro-level variables. Is there any information on additional data points, such as the cost of production? Researchers are working on determining a means to assess how costly bitcoins are to create for each of these organizations as more bitcoin miners go public and more research houses get involved in the field as it becomes more popular.

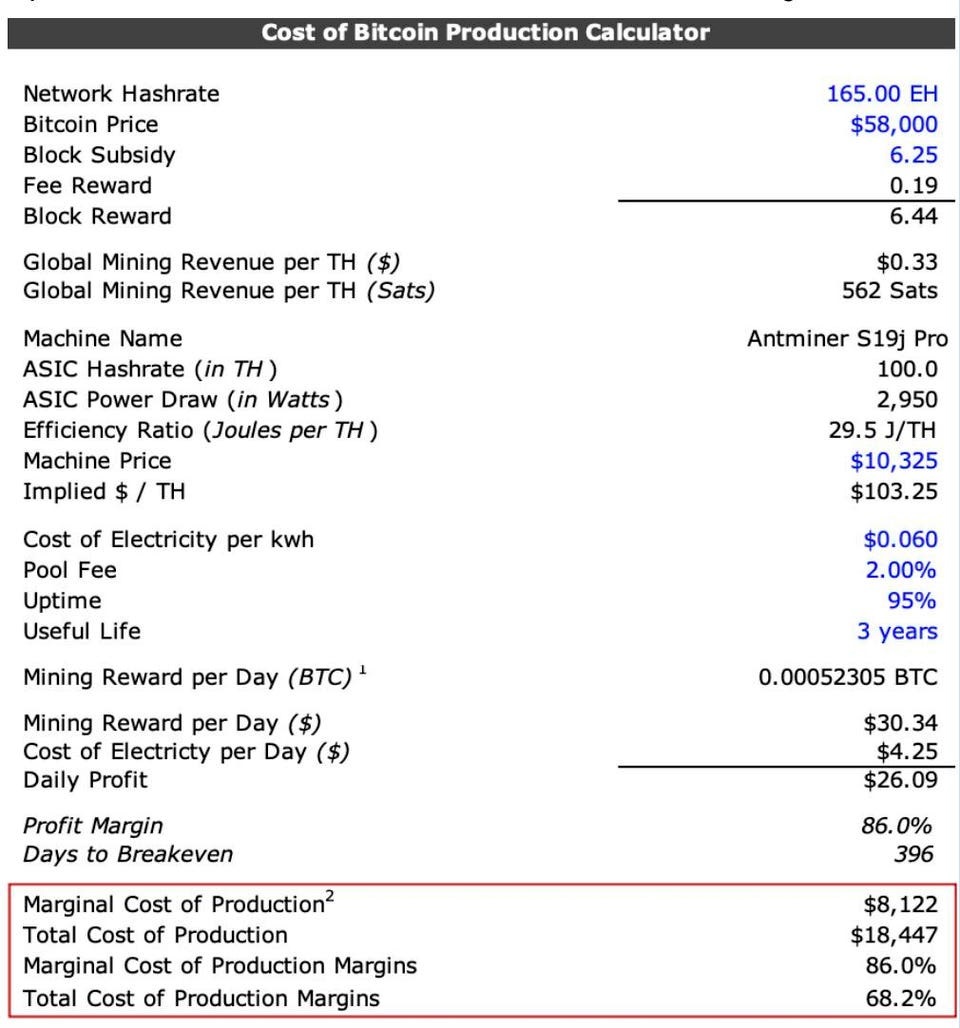

According to Amanda Fabiano, director of mining at Galaxy Digital, there is no commonly approved technique to data mining. ‘We discovered that when you look at publicly traded mining businesses, there are basically just a few KPIs that they all publish,” says the author. “It is comprised of the present hash rate, the anticipated future capacity, and the cost of mining a coin. So we looked a little more and discovered that everyone has a different method of calculating their cost per coin; the process is not really clear.”

The outcome was that Amanda and her team chose to develop their own methodology for computing the cost of a coin, based on information provided by firms in regulatory filings. It is done via three stages of analysis to break down the expenses into direct and indirect expenditures, while also taking into account depreciation and other factors. Before they start manufacturing, they compute a marginal cost of production that includes electricity and hosting fees, but does not include the cost of building a facility or purchasing new machinery. Second, they calculate the direct cost of manufacturing by factoring in a predetermined depreciation schedule to the total.

Of course, the depreciation of machines will vary based on their efficiency in use, their maintenance, and other factors, but Galaxy picked a three-year timeframe for depreciation purposes. By include the cost of labour, they are able to compile a comprehensive total cost of production. In addition to the study paper, the business is also making its model available for trial by the larger community through an Excel spreadsheet, which can be downloaded here.

“With the open-source worksheet, we really sought to create it in a manner that closely resembles one of those filers so people knew knew exactly what to look for, go to any firm they desired, pull up their filing, and insert it directly into our spreadsheet and have it automatically generate those different levels of the cost of production,” says Brandon Bailey, mining associate at Galaxy. Everyone can pick it up and do it since we made it as user-friendly as possible,” said the team.

So, what can we infer from this model? And what really is lacking? And anyway, like any good model, it relies on certain essential premises and eliminates some variables in order to concentrate on the most important data points to be considered. For example, Galaxy’s model does not take into account future mining capacity, money gained from price appreciation or the creation of balance sheet loans, or the relative efficiency of renewable energy sources vs fossil fuel energy sources, among other considerations.

Other analysts may use the models to include this into their work. Despite this, it still has some important points. For example, miners are beginning to use a variety of tactics in order to expand their operations. Marathon, for example, hosts the majority of its miners in third-party facilities and places a strong emphasis on leveraging its balance sheet to buy as much hashrate as possible.

Another kind of company, such as Riot, is far more vertically integrated since it has complete control over access to power sources as well as ownership of the buildings required to host the mining equipment.

One technique may not be superior to another, but according to Fabiano, “my hope is that the cost of mining a coin for vertically integrated firms would remain steady or drop over time.” “Assuming we are able to begin recording these indicators right once, we will be able to evaluate the effect of having your own infrastructure on the cost of power.”